By OliviaMorgan April 1, 2025

Credit card payments have come a long way since their early days. What was once a manual, time-consuming process involving carbon-copy machines and dial-up terminals is now fast, digital, and often contactless. As we step into 2025, small businesses are facing new trends, technologies, and expectations that are shaping the way credit card payments are handled.

Understanding this evolution isn’t just about keeping up—it’s about staying competitive, meeting customer expectations, and improving your bottom line. This article explores how credit card payments have evolved and what small business owners need to know to navigate the changes effectively.

A Look Back: How Credit Card Payments Have Changed Over Time

Credit cards have existed since the 1950s, but it wasn’t until the late 1980s and early 1990s that electronic payment systems became common. Initially, transactions were processed through manual imprinters, which required physical carbon copies of cards.

Then came magnetic stripe cards and point-of-sale (POS) terminals. This was a big leap forward, but it still required a customer to hand over their card and sign a receipt. By the early 2000s, chip cards emerged, offering greater security through EMV (Europay, Mastercard, and Visa) standards.

The real shift began with the growth of e-commerce and mobile technology. Contactless payments, digital wallets, and cloud-based POS systems began entering the mainstream. Now, in 2025, the payment landscape is driven by speed, security, convenience, and integration with digital experiences.

The Rise of Contactless and Mobile Payments

One of the most significant changes in recent years is the adoption of contactless payments. Whether it’s tapping a credit card or using a digital wallet like Apple Pay or Google Pay, customers now expect to pay quickly and without physical contact.

For small businesses, this means having terminals that support near-field communication (NFC) technology. Not only does this provide a smoother checkout experience, but it also speeds up transaction times and reduces lines—especially important for high-volume businesses like coffee shops, food trucks, and convenience stores.

Mobile payment options are also more popular than ever. Consumers use their smartphones and even smartwatches to complete purchases. As a result, businesses that can’t accommodate these methods risk losing customers to more tech-savvy competitors.

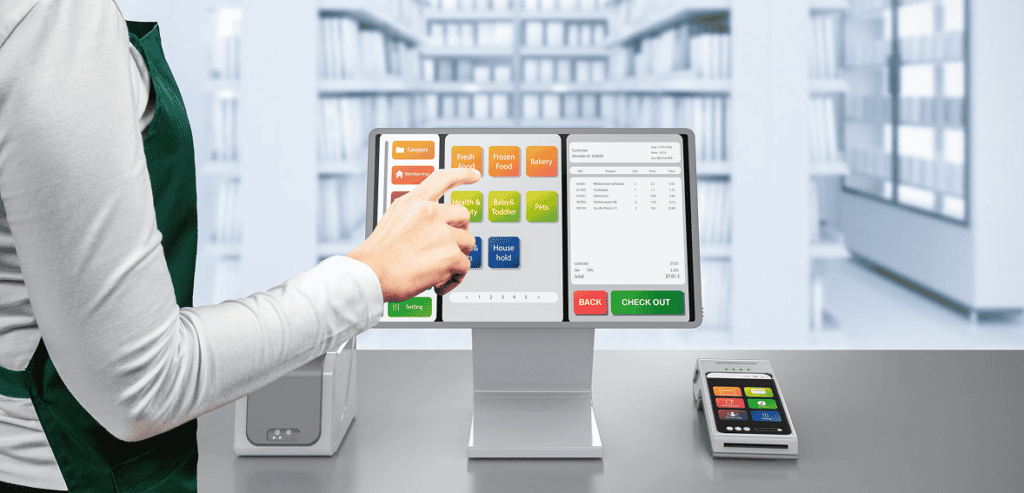

Integrated POS Systems: More Than Just a Payment Tool

Today’s credit card terminals are no longer just machines that process payments. Modern POS systems are full-service business tools that offer inventory management, customer relationship management, sales reporting, and even marketing tools.

These systems are increasingly cloud-based, which means they can be accessed from anywhere and updated in real time. For a small business, this kind of integration can save time, reduce errors, and provide valuable insights into customer behavior.

POS systems in 2025 are also highly customizable. Whether you’re running a bakery, boutique, or repair shop, there are platforms designed with your specific needs in mind. This level of personalization wasn’t available in the past, and it represents a huge leap forward in the evolution of credit card payments.

Subscription-Based Merchant Services

Another major change is how businesses now pay for credit card processing services. The traditional model was based on transaction fees—every time you processed a payment, a percentage and flat fee were deducted.

Now, many providers are offering subscription-based pricing, where businesses pay a monthly fee in exchange for lower (or even zero) per-transaction charges. For businesses that process a high volume of small-ticket items, this model can result in significant savings.

However, this model doesn’t suit everyone. Businesses with lower volume or seasonal traffic may still benefit from traditional pricing structures. The key is understanding your business’s transaction patterns and choosing a model that aligns with your financial goals.

The Growing Role of AI and Automation

Artificial intelligence is quietly transforming the payments industry. In 2025, many processors are using AI to detect fraud in real time, speed up authorizations, and personalize the customer experience.

For example, machine learning algorithms can flag unusual behavior patterns, such as a sudden spike in transactions or payments made from unusual locations. These tools help prevent chargebacks and reduce the risk of financial loss.

On the customer-facing side, AI is also being used to generate smarter receipts, offer instant loyalty rewards, and even suggest upsells based on past behavior. Small businesses that adopt AI-powered payment platforms are seeing increased engagement and better customer retention.

Biometric Verification and Enhanced Security

As cybersecurity threats continue to evolve, so do the technologies designed to fight them. In 2025, biometric verification is playing a larger role in credit card payments. Fingerprint scans, facial recognition, and even voice authentication are being used to confirm customer identities, especially for mobile and online transactions.

While this may sound futuristic, many consumers are already comfortable using biometrics to unlock their phones and authorize apps. Extending that experience to payments makes the process faster and more secure.

For small businesses, choosing a payment processor that prioritizes these security features is essential—not just for customer safety, but also for maintaining trust and complying with evolving data protection laws.

Digital Wallets Are the New Normal

Digital wallets have moved from being a niche convenience to a mainstream payment method. More customers now prefer using stored card information in apps like PayPal, Apple Pay, Samsung Pay, and Google Pay. This trend is especially prominent among younger consumers and those shopping online.

Digital wallets are valued for their ease of use, faster checkout, and reduced fraud risk. For small businesses, supporting digital wallets is no longer optional—it’s expected.

Offering digital wallet support can also reduce cart abandonment during online sales, speed up in-person transactions, and open your business to global customers who may not carry physical cards.

The Shift Toward Real-Time Payments

Traditionally, when a customer pays with a credit card, it can take one to three business days for the funds to reach the merchant’s account. But this delay is shrinking.

In 2025, real-time payments (RTP) are becoming more widespread, allowing businesses to access their funds within seconds or minutes after a transaction. This is particularly useful for businesses with tight cash flow, like restaurants, service providers, and freelancers.

Real-time settlements help you manage your expenses better, pay employees faster, and reinvest into your business more efficiently. As demand grows, more payment processors are beginning to offer this option—even for small business clients.

International Payments and Multi-Currency Support

The internet has made it easier than ever for small businesses to sell globally. But accepting payments from international customers still comes with some complications—currency conversion, higher fees, and longer settlement times.

Fortunately, many credit card processors in 2025 are providing better solutions for cross-border transactions. Some offer multi-currency pricing, allowing customers to pay in their local currency while you receive funds in your own. Others provide dynamic currency conversion, which lets you charge international customers without any manual adjustments.

Understanding the fees and regulations related to international payments is crucial if you plan to expand beyond local borders. Look for processors that offer clear, competitive rates and compliance with global security standards.

Buy Now, Pay Later (BNPL) Integration

Buy Now, Pay Later services like Afterpay, Klarna, and Affirm have become incredibly popular with consumers. These services allow customers to split purchases into smaller payments, often without interest. In 2025, these options are being built directly into credit card processing systems.

For small businesses, offering BNPL options can increase average order value and reduce cart abandonment. While there are fees associated with these services, the potential boost in revenue may outweigh the cost—especially for higher-ticket products or services.

Adding BNPL to your checkout process, both online and in-store, gives your customers more flexibility, which can set you apart from competitors.

The Importance of Transparent Reporting and Analytics

Gone are the days when payment processing meant simply checking your monthly statement. In 2025, credit card processors provide detailed analytics dashboards that give real-time insights into sales, transaction trends, and customer behavior.

For small businesses, this data is gold. You can track peak hours, best-selling items, customer return rates, and even compare performance across locations (if applicable). Having access to this kind of information helps you make smarter business decisions.

But not all providers offer the same level of reporting. When evaluating a credit card processor, consider the quality of its dashboard and the types of insights you can extract. The more data you can access, the better equipped you’ll be to grow your business.

Eco-Friendly and Paperless Payments

Sustainability is increasingly influencing consumer behavior. Many customers now prefer businesses that offer paperless receipts and eco-conscious practices.

Credit card payments in 2025 are more environmentally friendly than ever. Many POS systems now send digital receipts by text or email, reducing paper waste. Some also allow you to track your environmental impact by monitoring how much paper and energy your operations are saving.

Going paperless isn’t just good for the planet—it’s also good for business. It reduces supply costs, streamlines your checkout process, and supports your brand’s sustainability efforts.

Choosing the Right Payment Partner in 2025

With all the changes in how credit card payments work, choosing the right payment processor is more important than ever. It’s no longer just about cost—though that’s still a factor. You need a partner that can keep up with evolving technology, offer solid customer support, and scale with your business.

Here are some key factors to consider:

- Does the provider support contactless, mobile, and online payments?

- Are digital wallets and BNPL options included?

- What kind of reporting tools are available?

- How secure is the platform, and does it offer biometric or AI-powered fraud detection?

- Are the fees transparent and predictable?

Choosing a forward-thinking provider ensures that you won’t have to switch systems every year to keep up with new trends.

Final Thoughts

Credit card payments have come a long way, and in 2025, they continue to evolve faster than ever. For small businesses, keeping up with this evolution isn’t about adopting every new trend—it’s about making informed decisions that align with your goals and your customers’ expectations.

From contactless transactions to real-time payments, AI-driven fraud detection to integrated POS tools, the tools available today can empower your business in ways that weren’t possible even a few years ago.